Obstructive sleep apnea (OSA) affects roughly one out of every five people in the United States and it is estimated that 85% of people suffering from OSA are underdiagnosed (Santilli, et al., 2021). Obstructive sleep apnea is a respiratory disorder, wherein an individual’s airway is obstructed during sleep as muscles relax and the airway walls and tissue collapse. The resulting asphyxia arouses the individual from the deeper stages of sleep so that normal breathing can be restored. It is this disruption of regular sleep rhythms that causes the negative symptoms associated with sleep apnea. Because of this, diagnosing and treating sleep apnea is very important.

Obstructive sleep apnea (OSA) affects roughly one out of every five people in the United States and it is estimated that 85% of people suffering from OSA are underdiagnosed (Santilli, et al., 2021). Obstructive sleep apnea is a respiratory disorder, wherein an individual’s airway is obstructed during sleep as muscles relax and the airway walls and tissue collapse. The resulting asphyxia arouses the individual from the deeper stages of sleep so that normal breathing can be restored. It is this disruption of regular sleep rhythms that causes the negative symptoms associated with sleep apnea. Because of this, diagnosing and treating sleep apnea is very important.

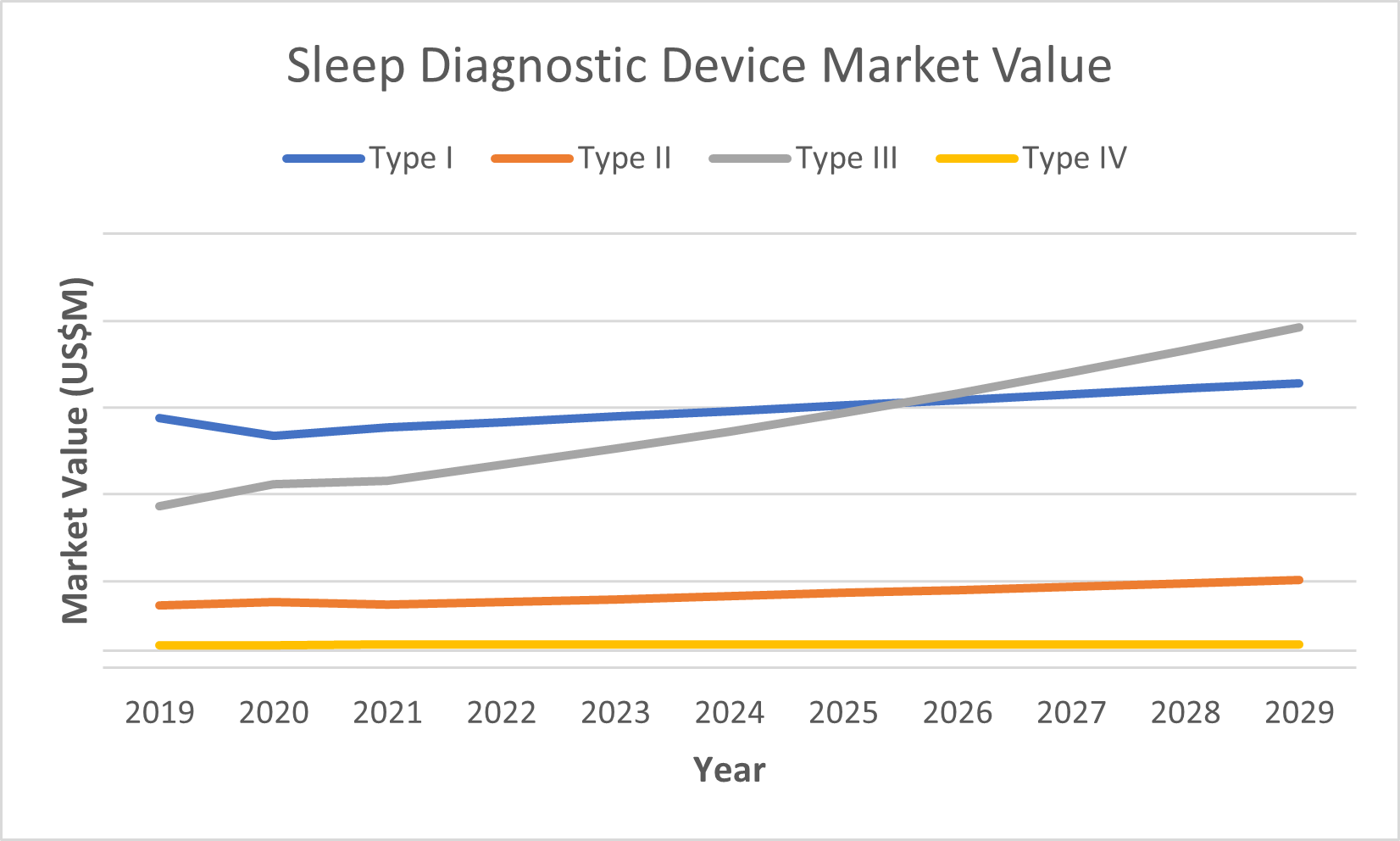

There are four main types of sleep diagnostics devices; type I device, type II device, type III device and type IV device. Type I devices are most complex, capable of performing a full, attended polysomnography (PSG) in a hospital or sleep test clinic setting. Types II, III and IV devices are home sleep tests (HSTs) and are less complex. Of the home sleep tests, type II devices are the most complex, capable of performing PSG without direct in-process monitoring from a sleep technologist, and are sometimes known as comprehensive portable devices. Type III devices do not describe sleep stages and sleep disruptions but provide enough information to a sleep doctor for a preliminary diagnosis of obstructive sleep apnea. Type IV devices are the simplest and least expensive devices and are used more as a low-cost screening tool instead of being used for diagnostic purposes.

Supply Chain Disruptions

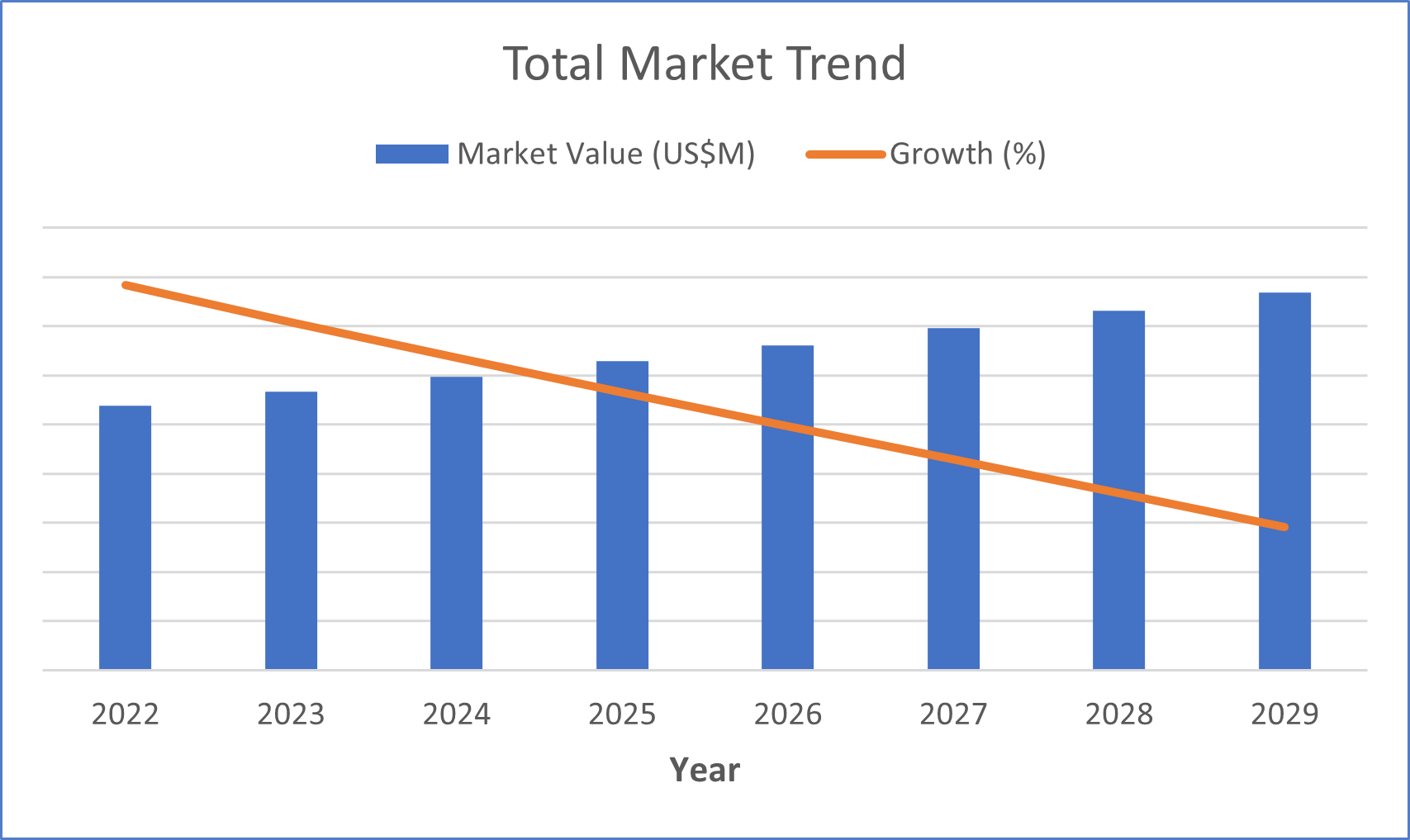

Because sleep apnea is so prevalent in the U.S., the sleep diagnostics market has continued to grow each year. The aging population and increase in average body weight, resulting in larger neck circumference and narrower airways, has fueled growth in this market (Mayo Clinic, 2023). Additionally, the general population is becoming more aware of sleep disorders. However, supply chain disruptions have limited this growth, preventing the market from capturing the entire demand of sleep diagnostics devices.

The three primary factors negatively impacting the supply chain for sleep diagnostics devices are chip shortages, the war in Ukraine and port delays related to the COVID-19 pandemic. As a result of these issues, average selling prices have generally increased in the market.

Chip Shortages

Integrated circuits, typically referred to as “chips,” are a collection of electronic components on a small chip used in electronic devices (sparkfun). In recent years, chips have been in short supply for numerous reasons, including a surge in the demand for electronics at the beginning of the pandemic when many people began working from home (Seeman, 2022). The more complex the device, the more chips are usually required to produce the product.

To make matters more difficult, the sleep diagnostics market is now competing with outside industries that use chips, perhaps the largest one being the auto industry. This adds another layer of hurdles, as some of these industries have more buying power and would more easily get a hold of the limited supply of chips.

War in Ukraine

The primary effect the war in Ukraine has had on the U.S. sleep diagnostics market is the prevention of acquiring raw materials to produce devices. Nickel and Palladium are some of the main raw materials disrupted by the war and are used in electronic devices (OECD, 2022). Correspondingly, prices for these have soared, causing vendors to increase prices, in turn affecting the sleep diagnostics market.

Shipping Delays

Worldwide, ports are understaffed mainly due to COVID-19 related layoffs (Stanley, 2022). Because of this, industries that rely on imports from overseas have been negatively impacted by shipping delays, increasing turnaround time. As a result, this affects how quickly vendors are able to receive and sell their products.

Impact on Each Device Type

Although the entire sleep diagnostics market is negatively impacted by these supply chain disruptions, the magnitude varies between the four device types.

Type I was impacted the greatest given that it is the most complex machine with numerous components, requiring more inputs. The shift to home sleep tests also negatively impacts growth in the type I market; however, the increase in more complex cases will mitigate these negative effects, as these patients will need professional assistance from the most complex test. As a result, growth is expected to be relatively flat for type I devices.

Type II is the most complex HST device, but is not as complex as type I devices. Prices in this market are increasing at a similar rate to type I devices; however, unit sales growth has not dropped to the same degree as in the type I market, as less materials are required to produce these devices.

Type III devices are much simpler than types I and II and were therefore less impacted. Type III devices are also becoming the most popular sleep diagnostics device, which has previously been the type I device. This trend was already apparent before the many supply chain disruptions, even to the point where most insurance plans required a patient to go through a type III device first to see if a type I test is necessary. As a result, type III devices were not significantly impacted by these disruptions and the type III device will continue to grow at the fastest rate.

Type IV devices are by far the simplest of sleep diagnostics devices and are even disputed about how reliable they are. As a result, this small segment of the sleep diagnostics market remained mostly unaffected.

Conclusion

The overall sleep diagnostics market is growing, especially due to the aging population and increase in average weight, both of which are highly correlated with obstructive sleep apnea (Mayo Clinic, 2023). However, supply chain disruptions, mainly chip shortages, the war limiting access to materials, and shipping delays, have greatly limited growth in this market.

For further insights, please see the report Anesthesia, Respiratory & Sleep Therapy Devices Market Size, Share & Trends 2023-2029 by iData Research.

About the Authors

Graham Diett is a research analyst at iData Research. He develops and composes syndicated research projects regarding the medical device industry, publishing the U.S. Anesthesia, Respiratory and Sleep Management Device report series.

Kamran Zamanian, Ph.D., is CEO and founding partner of iData Research. He has spent over 20 years working in the market research industry with a dedication to the study of medical devices used in the health of patients all over the globe.

About iData Research

For 17 years, iData Research has been a strong advocate for data-driven decision-making within the global medical device, dental, and pharmaceutical industries. By providing market research and consulting solutions, iData empowers its clients to trust the source of data and make important strategic decisions with confidence.

References

Mayo Clinic. (2023, April 6). Sleep Apnea. Retrieved from mayoclinic.org.

OECD. (2022, August 4). The Supply of Critical Raw Materials Endangered by Russia's war on Ukraine. Retrieved from oecd.org,

Santilli, M., Manciocchi, E., D'Addazio, G., Di Maria, E., D'Attilio, M., Femminella, B., & Sinjari, B. (2021, September 29). Prevalence of Obstructive Sleep Apnea Syndrome: A Single-Center Retrospective Study. Retrieved from ncbi.nlm.gov.

Seeman, D. (2022, April 27). What Caused the Global CHip Shortage? Retrieved from iotforall.com.

sparkfun. (n.d.). Integrated Circuits. Retrieved from learn.sparkfun.com.

Stanley, H. (2022, June 10). What Causes Shipping Delays? How They Impact Retailers and How to Deal With Them. Retrieved from shopify.com.